Investors looking for a disciplined, long-term method for choosing stocks frequently consider the rules established by famous fund manager Peter Lynch. His plan, explained in One Up on Wall Street, centers on finding firms with durable growth, good financial condition, and fair prices, a thinking often called Growth at a Reasonable Price (GARP). It stresses fundamental study instead of predicting market movements, looking for enterprises that are earning money, have manageable debt, and are valued at a price that matches their growth path without being too high. A recent filter using Lynch's main standards has pointed to Baker Hughes Co (NASDAQ:BKR) as a firm deserving more study.

Fit with Peter Lynch's Main Standards

The Peter Lynch filter uses particular, measurable rules to locate firms that match his investment thinking. Baker Hughes seems to satisfy a number of these important measures, which are made to find durable growth and financial soundness.

- Durable Earnings Growth: Lynch preferred firms increasing earnings per share (EPS) at a good, but not extreme, rate, usually between 15% and 30% each year over five years. This steers clear of trendy stocks with unstable growth. Baker Hughes states a five-year EPS growth rate of about 23.35%, putting it directly within this goal range and hinting at a record of steady, controlled increase.

- Fair Valuation using PEG Ratio: A key part of the Lynch method is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks where the price matches the growth rate. A PEG ratio at or under 1.0 is seen as good. Baker Hughes has a PEG ratio (using past five-year growth) of 0.77, suggesting the market might be pricing its shares at a point that does not completely account for its historical earnings growth.

- Good Profitability (ROE): Return on Equity (ROE) shows how well a firm produces profits from shareholder equity. Lynch wanted an ROE over 15%. Baker Hughes is above this level with an ROE of 15.92%, indicating capable management and a possibly lasting edge in its field.

- Cautious Financial Setup: To confirm strength, Lynch liked firms with sound balance sheets. His filters often ask for a Debt-to-Equity ratio below 0.6, and he personally favored an even smaller number. Baker Hughes reports a Debt-to-Equity ratio of 0.33, showing a careful capital structure using more equity than debt, which fits well with Lynch's focus on financial condition.

- Sufficient Short-Term Cash Flow: The Current Ratio checks a firm's capacity to pay its short-term bills. A ratio of 1 or more is normally seen as acceptable. Baker Hughes has a Current Ratio of 1.41, meaning it has enough liquid assets to cover its upcoming debts, another positive for financial soundness.

Fundamental Condition and Growth Picture

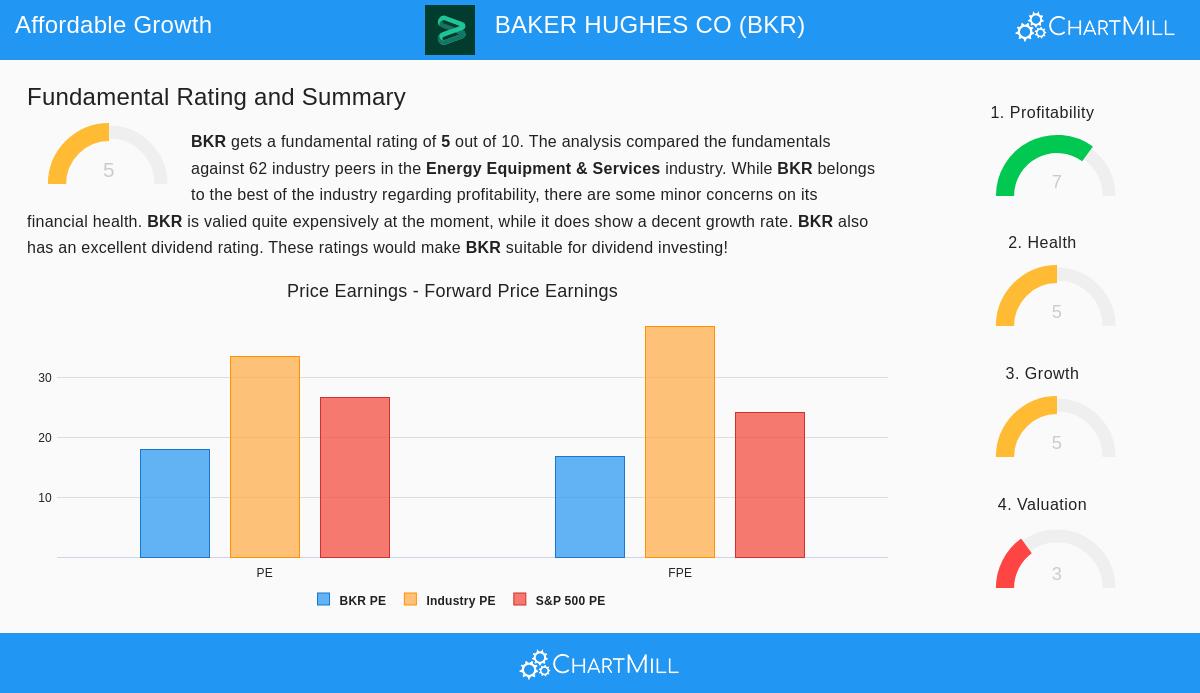

A wider view of Baker Hughes's fundamental study report gives background beyond the filter's rules. The firm gets an overall fundamental score of 5 out of 10, showing a varied but notable picture when measured against similar firms in the Energy Equipment & Services industry.

- Profitability is a Definite Positive: The company gets a 7 out of 10 for profitability. Main points include field-leading numbers for Return on Assets (7.37%) and Profit Margin (10.43%), with both operating and profit margins displaying upward movements in recent years.

- Dividend Attraction: For investors focused on income using GARP ideas, the dividend picture is interesting, scoring a 7. The firm gives a yield of 2.07% with a maintainable payout ratio near 31% and a steady history of at least ten years of regular payments without a cut.

- A Moderate Stance on Condition and Valuation: The financial condition score is a neutral 5. While the low debt level is a plus, liquidity ratios (Current and Quick Ratio) are seen as smaller than many industry counterparts. The valuation score is a 3, mainly because of what the report calls a high PEG ratio. Still, it is key to see that this view might use a different PEG math; the filter's found PEG of 0.77 using past growth shows a more positive image. The normal P/E ratio of 17.96 is also viewed as less expensive than both the S&P 500 average and the industry average.

- Stable Growth Path: The growth score is a 5. The firm shows very good past EPS growth (23.35% yearly) and is predicted to provide solid future EPS growth of about 10.41%, though at a slower speed. Revenue growth is forecast to be steady but small in the low single digits.

For a complete look at these numbers, you can see the full fundamental analysis report for BKR.

Investment Points

For investors who agree with Peter Lynch's thinking, Baker Hughes offers an example of a GARP investment in the industrial energy technology and services field. It meets several of Lynch's tests: decent historical growth in a maintainable range, a price that seems fair when growth is considered (PEG < 1), high profitability, and a very strong balance sheet with little debt. The extra part of a dependable and increasing dividend adds to its attraction for long-term, buy-and-keep portfolios.

However, Lynch's plan also needs knowing the business. Possible investors must judge if Baker Hughes's place in the shifting energy environment, covering traditional oilfield services and newer lower carbon options, supports ongoing growth and profit steadiness. The firm's future relies on its skill to manage the energy shift, making non-quantitative study necessary.

Find Other Possible Investments

Baker Hughes came from a specific filter based on Peter Lynch's standards. If this way of thinking matches your investment plan, you can locate other firms that pass these same rules by using the Peter Lynch Strategy stock screener. Recall, a filter gives a beginning for study, not a list to buy. Following Lynch's suggestion, the following action is complete careful checking to know each business before thinking about an investment.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or a deal to buy or sell any security. Investing has risk, including the possible loss of original money. You should do your own study and talk with a qualified financial advisor before making any investment choices.