For investors looking for chances where the market price may not completely show a company's true value, a methodical screening process can help find possible candidates. One method is to look for stocks that show a solid fundamental valuation score, meaning they are priced cautiously compared to their financials, while also holding acceptable scores in profitability, financial health, and growth. This mix tries to find companies that are not just low-priced, but low-priced without a clear cause, possibly providing a buffer for strategies focused on value.

Best Buy Co Inc (NYSE:BBY), the consumer electronics retail leader, comes from such a screen as a stock deserving more examination. The company’s latest fundamental analysis report describes a mature, profitable business trading at a notable discount to the wider market, all while giving large amounts of capital back to shareholders.

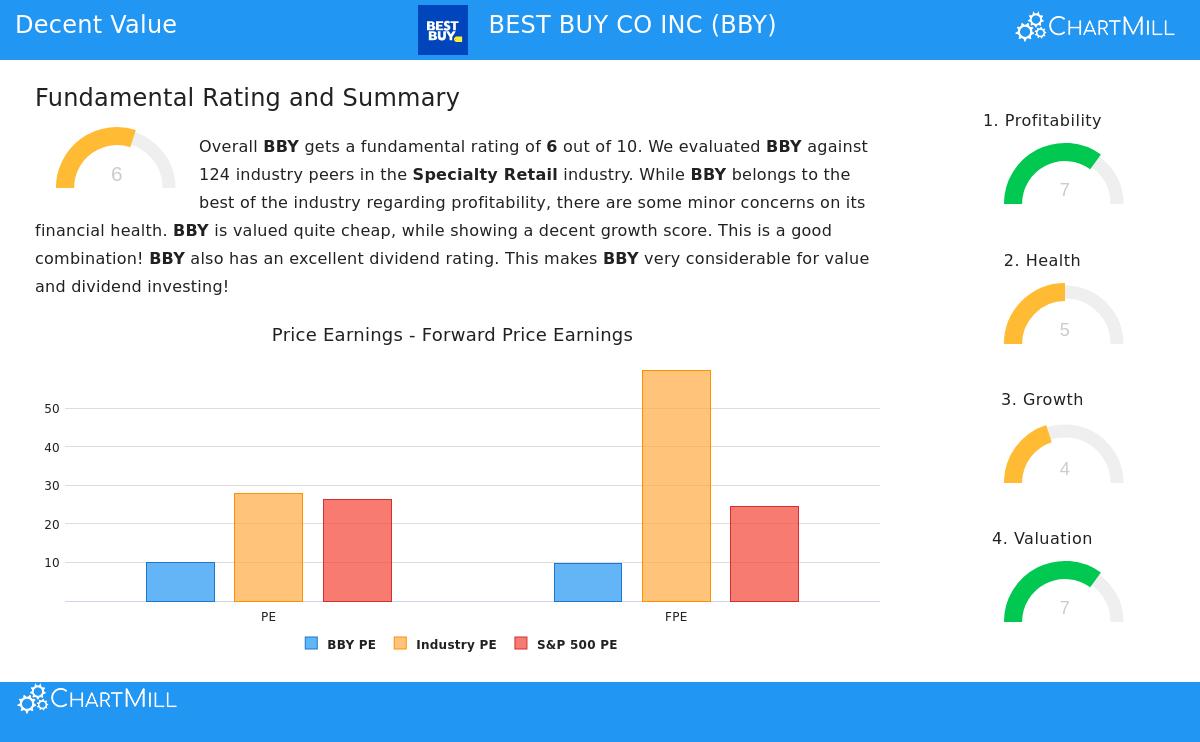

Valuation: A Clear Discount

The central idea of value investing is buying assets for less than their true worth. Best Buy’s valuation numbers point to a notable gap between its market price and its financial results, a main beginning point for value investors.

- Price-to-Earnings (P/E): With a trailing P/E ratio of 10.06, BBY trades at a large discount to both the S&P 500 average (26.25) and its industry group in Specialty Retail (average 27.89). Its forward P/E of 9.63 shows a comparable situation.

- Enterprise Value to EBITDA & Price/Free Cash Flow: The company also looks inexpensive on these cash-flow based measures, ranking more reasonably than about 90% and 79% of its industry rivals, in turn.

- Dividend Yield: A notable 5.82% yield not only greatly surpasses the industry average of 2.36% and the S&P 500’s 1.82%, but also gives a real return while investors wait for a possible valuation change.

This overall valuation view backs the screen’s main filter, showing BBY is priced cautiously. For a value investor, these numbers can mark a chance if the low price is not explained by worsening business fundamentals.

Profitability & Financial Health: The Base of Safety

A low-priced stock is only a sound investment if the company is fundamentally healthy. Value methods stress the need for a solid financial base to provide that important buffer. Best Buy’s report displays strong points here, though with some detailed aspects.

Profitability is a clear area of strength. The company receives a high grade based on outstanding returns on capital:

- Return on Invested Capital (ROIC) of 18.65% is better than 87% of the industry.

- Return on Equity of 36.07% is with the top in its sector.

- The company has been steadily profitable with positive cash flow for more than five years.

These numbers show management’s effectiveness in creating profits from the capital it uses, a mark of a good business often wanted by value investors.

Financial Health shows a more varied, but generally steady, picture. Solvency is very good, with an extremely low debt-to-free-cash-flow ratio of 0.93, indicating the company could pay off all its debt in under a year from its cash flow. Its debt-to-equity ratio is also acceptable at 0.39. However, liquidity ratios (Current and Quick Ratios) are noted as points of attention, ranking below many peers. This implies investors should watch the company’s working capital management, though its solid cash generation lessens near-term liquidity concerns.

Growth: A Stabilizing View

Strict value stocks frequently have limited growth, but some forward movement can help drive a re-rating. Best Buy’s growth picture has faced difficulties, with Revenue and EPS showing small decreases on average over recent years. However, the report points to a positive change expected next.

- Analysts estimate EPS growth to increase to almost 11% each year in the coming years.

- Revenue growth is also predicted to become positive, though at a moderate rate.

- The report specifically states that both EPS and Revenue growth rates are increasing compared to the past.

This expected shift from contraction to growth is important. It suggests the company is managing a post-pandemic adjustment and may be moving past cyclical pressures, giving a possible trigger that value investors search for beyond simple low price.

Conclusion & Further Research

Best Buy shows an example of a possible value case: a top company with strong profitability and shareholder returns, trading at a reduced valuation because of seen growth issues. The fundamental report implies those issues may be lessening, with growth estimated to increase again. The high dividend yield gives payment for the wait.

This review of BBY came from a systematic search for acceptable value stocks. If this method fits your investment style, you can investigate more possible candidates using the same Decent Value Stocks screen.

Disclaimer: This article is for informational and educational purposes only and does not form financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and grades given by ChartMill, and investors should do their own research and talk with a qualified financial advisor before making any investment decisions. Past performance is not a guide to future results.