For investors looking for chances where a company's market price may not completely show its basic strength, a methodical value method can be a useful structure. This process involves searching for companies that seem basically priced low by common measures while still showing good financial condition, steady earnings, and acceptable expansion potential. The aim is to find possible differences between a stock's present price and its real business worth, offering a buffer for the patient investor.

Barrick Mining Corp (NYSE:B), one of the biggest gold and copper producers globally, comes from such a search as a candidate for more detailed review. The company's most recent fundamental analysis report shows a financially sound business trading at what seems to be a lower price compared to both its sector and its own operational standard.

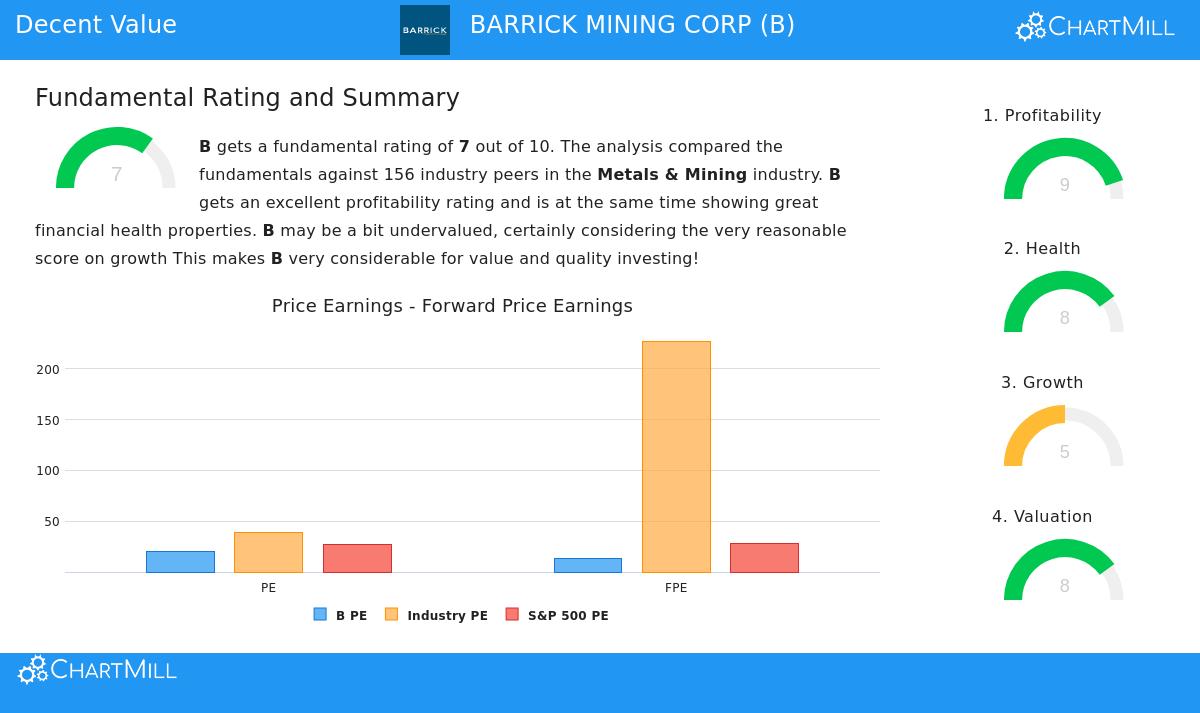

Valuation: An Interesting Entry Point

The central idea of value investing is buying an asset for less than its calculated value. Barrick's valuation measures indicate the market may be valuing the company cautiously.

- Relative Value: While Barrick's own Price-to-Earnings (P/E) ratio of 20.64 may look high, the situation is important. This number is much lower priced than 83% of similar companies in the Metals & Mining sector, where the average P/E is above 38. This sector-relative lower price is a clear value indicator.

- Future and Cash Flow Measures: The valuation view improves with future and cash-based measures. The company's Price-to-Forward Earnings ratio of 13.23 and its Enterprise Value-to-EBITDA ratio are lower priced than about 81% and 89% of industry rivals, in turn. Also, its Price-to-Free Cash Flow ratio is more appealing than almost 90% of the industry, showing the market is paying less for each dollar of cash Barrick produces.

- Supported by Basics: Significantly, this lower valuation is not linked with poor basics. The report states that Barrick's "excellent profitability score" and anticipated earnings expansion could support a higher multiple, implying the present price might not completely include these positives.

Financial Health: A Secure Balance Sheet

A secure financial base is essential for value investors, as it offers durability during economic slowdowns and lowers failure risk. Barrick scores well here, with a Health score of 8 out of 10.

- Solvency: The company keeps a careful debt structure, with a low Debt-to-Equity ratio of 0.17, showing a good balance between funding sources. Even more notable is its Debt-to-Free Cash Flow ratio of 1.22, meaning it could pay off all its debt with just over a year of its cash flow—a situation better than 81% of its sector.

- Liquidity: Barrick shows sufficient short-term financial room. Its Current Ratio of 2.92 and Quick Ratio of 2.33 are well above the level seen as good, showing no trouble in meeting immediate responsibilities and doing better than most mining companies.

Profitability: High-Standard Operations

Value is not only about a low price; it is about buying a good business at that price. Barrick's outstanding Profitability score of 9 out of 10 confirms it is a very efficient operator.

- Good Returns: The company produces appealing returns on capital. Its Return on Equity (ROE) of 18.80% and Return on Invested Capital (ROIC) of 12.40% put it in the best group of its sector, doing better than 89% and 83% of peers, in turn. This shows management is using shareholder capital well.

- Secure Margins: Barrick's operational effectiveness is clear in its margins. An Operating Margin of 47.45% and a Profit Margin of 29.45% are some of the best in the industry, doing better than over 90% of rivals. These margins have also shown positive movement in recent years, a sign of better operational management.

Growth and Dividend: A Supportive Setting

While not a pure expansion story, Barrick offers a supportive setting of growth and shareholder returns, which can improve total return for a value investor.

- Past Results: The company has provided good recent expansion, with Earnings Per Share (EPS) rising 92% over the last year and Revenue increasing by over 31%. Its longer-term history shows an average yearly EPS expansion of 16.24%.

- Future Outlook and Income: Looking forward, analysts anticipate moderate expansion to continue. The dividend, while providing a modest 0.88% yield, has a good history of growth at over 10% each year and is backed by a maintainable payout ratio of less than 18% of earnings, leaving plenty of room for reinvestment and further rises.

Conclusion

For investors using a value-focused method, Barrick Mining Corp offers an interesting case. It seems to be a financially secure company with first-class profitability that is presently trading at a lower price compared to its own sector. The mix of a secure balance sheet, excellent margins, and an acceptable valuation forms the kind of profile value investors frequently look for: a high-standard business that may be briefly priced low by the wider market. This agreement of points indicates the stock's present price may not completely show the basic strength and steadiness of its global mining activities.

Find More Possible Value Choices The review of Barrick Gold came from a methodical hunt for acceptable value stocks. If you want to examine other companies that fit similar conditions of good valuation, health, profitability, and expansion, you can view the prepared screen here.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer or request to buy or sell any securities. The information shown is based on supplied data and should not be the only foundation for any investment choice. Investing includes risk, including the possible loss of initial funds. Always do your own research and think about talking with a qualified financial advisor before making any investment choices.