The search for quality investments is a central part of long-term portfolio construction. Unlike purely value-driven strategies, quality investing centers on finding companies with lasting competitive strengths, sound financial condition, and the capacity to produce steady, high-returns on capital. These are the businesses an investor can confidently own for decades. One systematic method for locating such companies is the "Caviar Cruise" stock screen, a process built on ideas from quality investing that selects for firms with solid historical growth, high profitability, and strong financial foundations. This screen focuses on measurable data like maintained revenue and profit growth, high returns on invested capital, reasonable debt levels, and high-quality earnings that become free cash flow.

A recent run of this screen has identified Broadcom Inc (NASDAQ:AVGO) as a leading example. The global technology leader in semiconductors and infrastructure software seems to display many of the features quality investors look for. We can look at how Broadcom's financial profile matches the main selections of the Caviar Cruise method.

Matching the Main Quality Standards

The Caviar Cruise screen uses a set of strict selections to find companies with outstanding operational and financial traits. Broadcom's reported numbers not only match but greatly surpass the minimum standards.

-

Historical Growth: The screen calls for a minimum 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. It also requires that profit growth exceeds sales growth, pointing to better operational efficiency and pricing ability. Broadcom performs well here, with a 5-year revenue CAGR of 29.08% and a notable EBIT CAGR of 43.11%. This large difference confirms the company's capacity to turn top-line growth into even quicker bottom-line increase.

-

Profitability and Capital Efficiency: A main idea of quality investing is exceptional capital use. The screen demands a Return on Invested Capital (excluding cash, goodwill, and intangibles) above 15%. Broadcom's number of 257.21% is very high, indicating the company produces great profit from each dollar put into its core business activities. This is a clear sign of a strong competitive position and good management performance.

-

Financial Soundness and Earnings Quality: Quality companies should not carry too much debt. The screen employs a Debt-to-Free Cash Flow ratio below 5, showing how many years of current cash flow would be required to settle all debt. Broadcom's ratio of 2.42 points to a comfortable and workable debt load. Also, the screen checks for "high-quality" profits by requiring that, on average, at least 75% of net income becomes free cash flow over five years. Broadcom's average Profit Quality of 184.64% is much higher than this, showing very strong cash generation that goes beyond its accounting profits—a clear mark of financial soundness.

Broadcom's Fundamental Profile in Summary

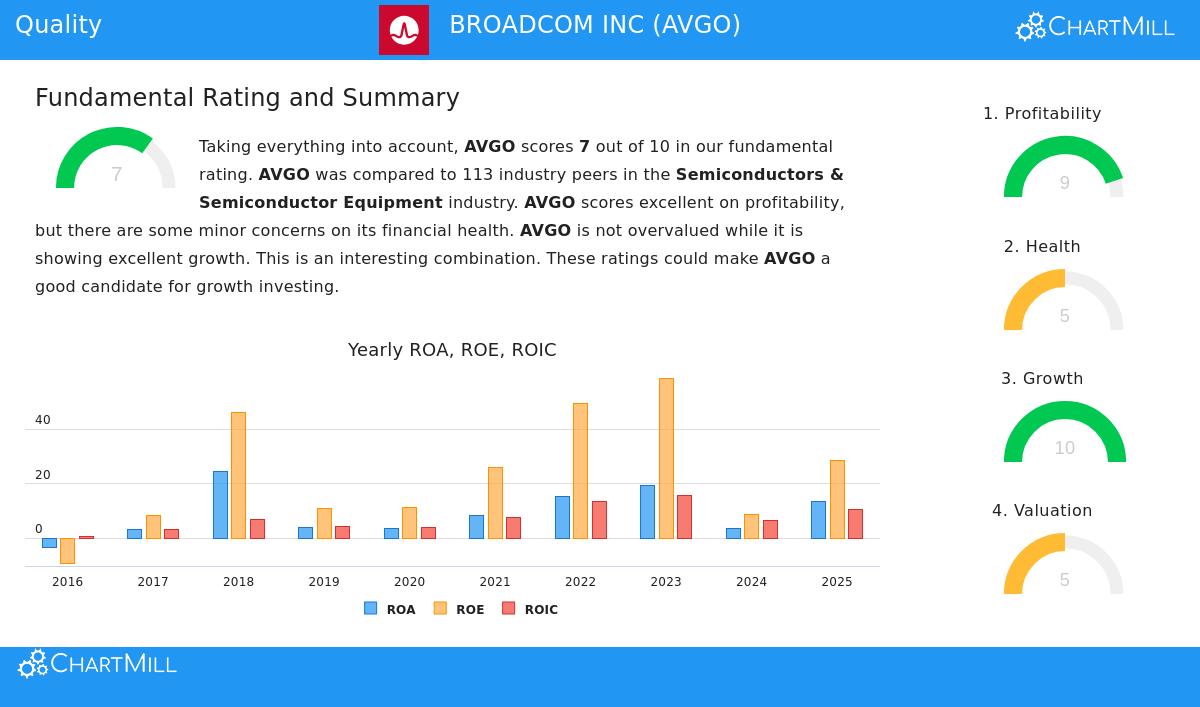

A look at Broadcom's detailed fundamental analysis report supports the image shown by the screen. The company receives a solid overall fundamental score of 7 out of 10, with specific high points in growth and profitability.

- Profitability is a main positive, scoring a near-maximum 9/10. The company has industry-leading margins, with a Profit Margin of 36.20% and an Operating Margin of 40.94%, each beating over 95% of its semiconductor industry competitors. These margins have also shown steady improvement.

- Growth numbers are outstanding, scoring a maximum 10/10. Broadcom has shown strong historical growth in both revenue and earnings per share, and analysts expect this solid trend to persist.

- Valuation offers a varied view, scoring a middle 5/10. While traditional P/E ratios seem high, measures like the Price/Free Cash Flow ratio are more attractive compared to the industry. The report states that the company's high growth and profitability may support its higher valuation for some investors.

- Financial Condition is acceptable with a score of 5/10, though it is the area with some smaller points to note. While the company's Altman-Z score indicates very low bankruptcy risk and its Debt-to-FCF ratio is positive, its liquidity ratios (Current and Quick Ratio) are below many industry peers. The company's debt level, while workable, is above average for the sector.

Is Broadcom a "Buy-and-Hold" Quality Stock?

For an investor using a quality-focused, buy-and-hold plan, Broadcom offers a strong argument. It works in the necessary technology infrastructure field, supplying key semiconductors and software—a market with a definite long-term growth direction. Its very high ROIC and increasing margins suggest a strong competitive edge and pricing ability. The company's capacity to grow earnings quicker than revenue and turn those earnings into significant free cash flow supplies the financial means for ongoing innovation, strategic purchases, and shareholder returns, as shown by its steady and rising dividend.

The Caviar Cruise screen is made to find companies deserving of thorough, long-term study, and Broadcom's success through its selections makes it a notable example for such examination. The screen's attention on lasting profitability, efficient growth, and financial stability matches directly with the qualities that help a business last and increase value over many years.

You can review the present list of stocks passing the Caviar Cruise quality screen for yourself here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own thorough research and consult with a qualified financial advisor before making any investment decisions.