Investors looking for growth opportunities often face a dilemma: high-growth companies frequently trade at premium valuations, raising the risk of paying too much for future potential. A strategy to address this is the "Affordable Growth" or "Growth at a Reasonable Price" (GARP) approach. This method seeks to identify companies that are not only expanding quickly but also possess good underlying fundamentals, all while being priced at a level that does not fully account for years of future success. By screening for stocks with solid growth ratings, acceptable profitability and financial health, and a valuation that is not too high, investors aim to find a balance between opportunity and caution.

Atour Lifestyle Holdings Ltd. (NASDAQ:ATAT) appears as a candidate from such a screening process. The Chinese hotel operator, with a portfolio including brands like Atour, Atour Light, and ZHOTEL across more than 150 cities, has demonstrated a strong fundamental profile that fits this investment philosophy.

Strong Growth Path

The central idea of an affordable growth strategy is, unsurprisingly, growth. ATAT shows good momentum on this front, earning a high Growth Rating of 9 out of 10 from ChartMill. The company's expansion is not a recent event but a continuing trend.

- Revenue Growth: Over the past year, revenue increased by 36.24%, with an average yearly growth rate of nearly 36% over recent years. This points to a steady and consistent enlargement of its hotel network and customer base.

- Earnings Power: While earnings per share (EPS) grew a modest 5.07% in the last year, the average yearly EPS growth over a longer period is a notable 138%. This implies the company is moving into a phase of highly profitable scaling.

- Future Expectations: Analysts expect this solid performance to continue, with estimated forward EPS growth of 24.88% and revenue growth of 27.00% yearly. This forward-looking confidence is important for a GARP investment, as it provides a path for the company's current valuation.

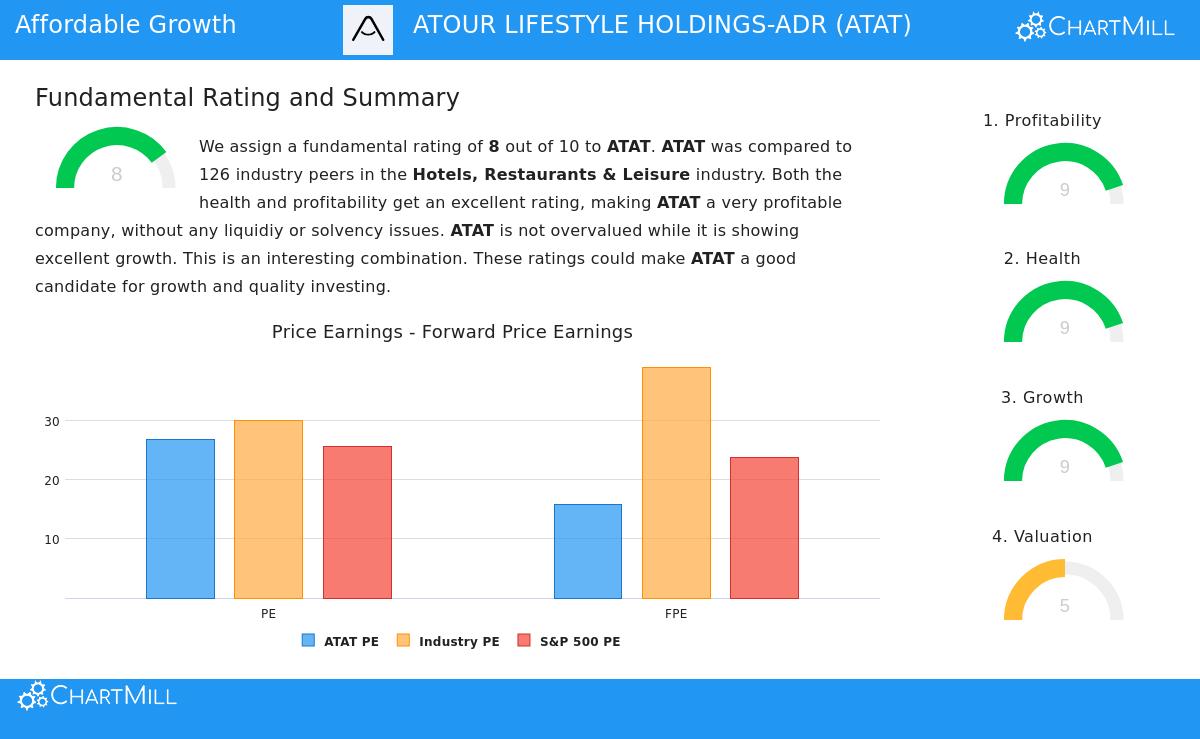

Valuation in Perspective

A fair valuation is what distinguishes an "affordable" growth stock from a costly one. ATAT receives a Valuation Rating of 5, which meets the screen's requirement and indicates a balanced, market-aligned price. The analysis shows a detailed picture.

- P/E Ratio: With a trailing Price-to-Earnings (P/E) ratio of 26.90, ATAT trades similarly to the broader S&P 500 average (25.71) and is actually less expensive than many peers in the Hotels, Restaurants & Leisure industry, which has an average P/E above 30.

- Forward-Looking Metrics: The valuation appears more attractive on a forward-looking basis. The Price/Forward Earnings ratio of 15.89 is clearly lower than both the S&P 500 average (23.83) and the industry average. Also, its Price/Free Cash Flow ratio is lower than about 77% of its industry competitors.

- Growth Adjustment: The low PEG ratio, which modifies the P/E for expected growth, signals the market may not be fully accounting for ATAT's projected earnings expansion. This is a notable point for GARP investors, implying the growth narrative may be available at a fair price.

Supporting Fundamentals: Health and Profitability

Lasting growth cannot exist without a firm base. This is why the affordable growth screen also filters for acceptable profitability and financial health, to avoid companies growing unsustainably through too much debt or poor operations. ATAT performs well here, with a Profitability Rating of 9 and a Financial Health Rating of 9.

Profitability Quality:

- The company shows very good margins, including a Gross Margin of 82.68% (better than 95% of its industry) and an Operating Margin of 22.20%.

- Its efficiency in using capital is significant, with a Return on Invested Capital (ROIC) of 25.73%, higher than 95% of industry peers.

Financial Health Quality:

- Solvency is solid, with a very low Debt/Equity ratio of 0.02 and a small Debt to Free Cash Flow ratio of 0.04, meaning it could pay off all debt in a short time from its cash flow.

- Liquidity is good, with Current and Quick Ratios above 2.0, giving ample room to meet short-term obligations.

These high scores in health and profitability give important perspective to the growth and valuation metrics. They show that ATAT's expansion is supported by efficient operations and a strong balance sheet, lowering the fundamental risks often linked with high-growth stocks.

Conclusion

Atour Lifestyle Holdings presents a profile that matches the affordable growth investment strategy. It combines a solid, proven growth record with positive future projections. While its trailing P/E is not very low, forward-looking metrics and its low PEG ratio imply the market may be offering its growth narrative at a fair entry point. Most importantly, this growth is supported by very good profitability and firm financial health, addressing main risk factors for investors.

For investors interested in examining other companies that meet similar standards of good growth, fair valuation, and sound fundamentals, more results can be found by using the Affordable Growth stock screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data provided and fundamental ratings from ChartMill. Investors should conduct their own research and consider their individual financial circumstances before making any investment decisions. You can view the full fundamental analysis report for ATAT here.