For investors looking for chances where a company's market price seems separate from its actual business condition, a systematic value investing method can be a useful path. This strategy, made famous by Benjamin Graham and Warren Buffett, focuses on finding stocks selling for less than their calculated worth while still displaying good basic condition. One useful method is to search for companies that rate well on price measures but also keep acceptable ratings in earnings, balance sheet soundness, and expansion, confirming the low price is not a pitfall but a possible chance. A recent search for these "acceptable value" stocks has pointed to APA CORP (NASDAQ:APA) as a candidate needing more examination.

Examining the Fundamental Report

A thorough fundamental analysis report for APA gives an organized, number-based view across five key sections: Valuation, Profitability, Financial Health, Growth, and Dividend. For a value investor, this separation is important. An inexpensive stock is only a worthwhile purchase if the company is basically healthy and can continue; if not, it could be a "value trap" where low prices indicate lasting problems instead of short-term market doubt. APA's total fundamental score of 6 out of 10, compared to others in the Oil, Gas & Consumable Fuels industry, indicates a varied but interesting picture, with definite positives in particular sections that match value-focused standards.

Valuation: The Heart of the Chance

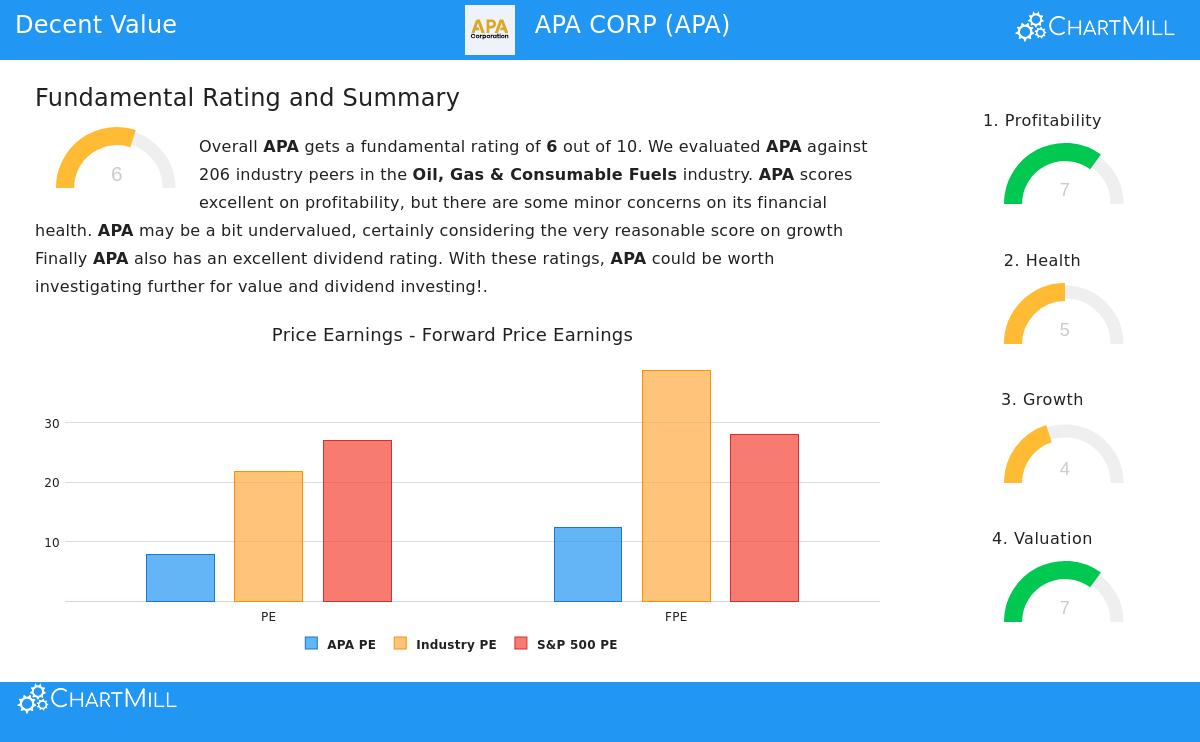

The main attraction for a value investor is a stock with a notably low price. APA's price measures are its most notable aspect, receiving a ChartMill Valuation Rating of 7.

- Price-to-Earnings (P/E) Ratio: At 7.84, APA's P/E ratio is low next to the S&P 500 average of about 27 and also makes it less expensive than over 90% of similar companies.

- Enterprise Value to EBITDA & Price/Free Cash Flow: The company is priced lower than 96.6% and 98.06% of its industry using these measures, showing the market gives a low value to its ability to produce cash.

- Context: This low price is the beginning. The value method depends on purchasing such discounts, if the company's business is healthy enough to finally reduce the difference between price and calculated worth.

Profitability and Financial Health: Evaluating the Base

A low price is not important if the company loses money or has a weak balance sheet. APA displays a good profitability picture with a rating of 7, meaning its business runs effectively.

- Strong Earnings: The company has a very good Return on Invested Capital (ROIC) of 14.25% and a Return on Equity of 25.30%, doing better than most of its industry. This shows management uses money well to create earnings.

- Good Margins: With an Operating Margin of 30.75% and a Gross Margin of 69.21%, APA keeps good price control and cost management compared to others.

Financial Health, with a rating of 5, shows a more detailed picture but with important balancing factors.

- Solvency Positives: APA's debt is very well covered by its free cash flow (Debt/FCF ratio of 0.94), meaning it could pay all debt in under a year from its cash, a situation better than 88% of similar companies. Its ROIC is also higher than its cost of capital, proving it builds value for shareholders.

- Liquidity Points to Watch: The report mentions lower short-term liquidity ratios (Current and Quick Ratios under 1), which is typical in the energy field but needs attention. The good point is that the company's solid free cash flow offers protection against these near-term needs.

Growth and Dividend: The Possible Drivers

For the price difference to shrink, a company needs some forward progress. APA's Growth rating is a middle 4, showing a change period.

- History vs. Outlook: The company has demonstrated very strong past EPS and sales growth. However, predictions have softened, with analysts expecting a small drop in earnings next year with little sales growth. This probably adds to its low price.

- Income Part: APA does well with a Dividend rating of 7. Its yield of 3.44% is good, backed by a manageable payout ratio of only 24% of earnings. A steady, well-supported dividend gives a real return while investors wait for possible price growth, a standard value investing advantage.

Conclusion: A Value Case in Energy

APA CORP shows an example of measured value searching. It is clearly low-priced on common valuation measures, meeting the main idea of looking for a price buffer. Importantly, this low price is connected to a company that stays very profitable and creates large free cash flow, which backs its dividend and debt handling. While near-term growth outlooks are quiet and liquidity numbers need observation, the fundamental report indicates the current price may not completely show the company's ability to generate cash and balance sheet strength.

For investors wanting to study similar chances that mix good price with acceptable basic condition, more study can start with the Decent Value Stocks screen used to find APA.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of money. You should do your own study and talk with a qualified financial advisor before making any investment choices.