For investors looking for reliable income, a methodical screening process can help find companies that provide more than a high stated yield. A frequent method involves selecting for stocks that join a firm dedication to shareholder payouts with basic business soundness. This frequently means searching for companies with a high dividend rating, which assesses the yield, growth, and durability of the dividend, while also confirming they have acceptable profitability and financial soundness. This method tries to steer clear of "yield traps," companies with unmaintainably high yields frequently caused by a falling stock price, and instead concentrates on firms with the operational and financial strength to keep and raise their dividends over time.

One company that appears from such a screen is SMITH (A.O.) CORP (NYSE:AOS), a top producer of water heating and water treatment products. The company’s basic profile indicates it merits more examination from dividend-oriented investors, as it seems to combine a satisfactory income stream with a solid operational base.

Examining the Dividend Profile

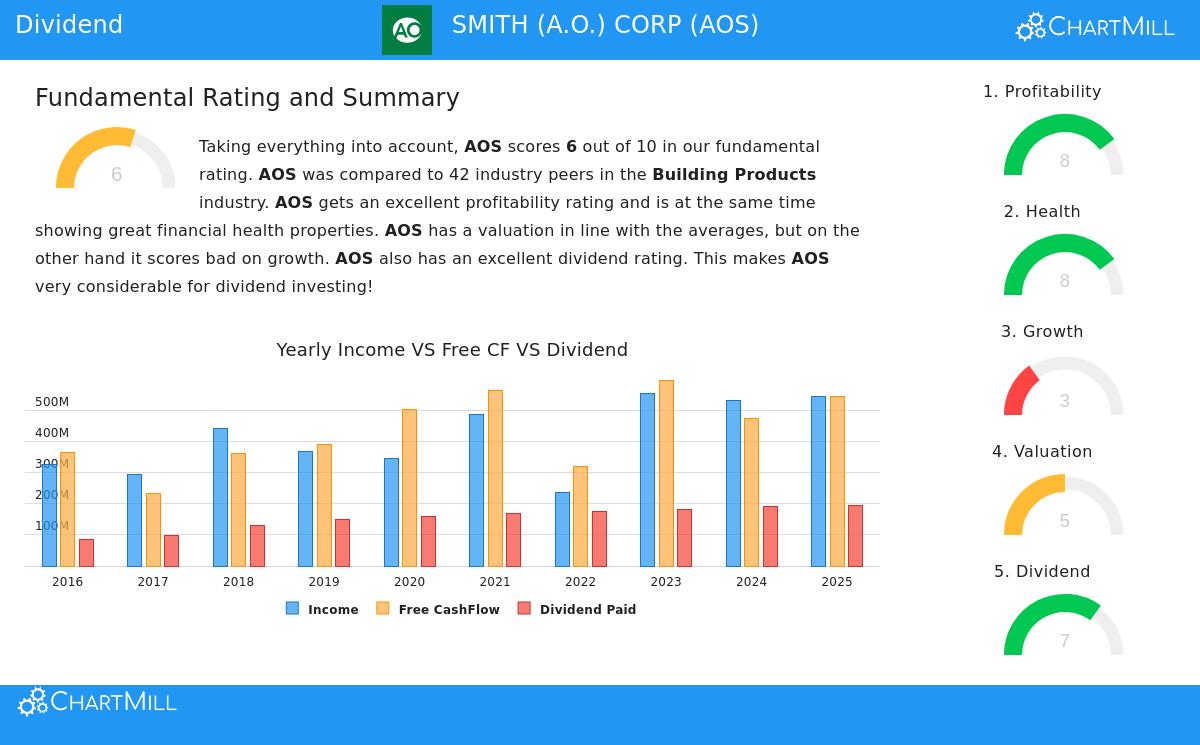

The center of the investment case for A.O. Smith is in its shareholder return policy, which receives a good 7 out of 10 on the ChartMill Dividend Rating. This rating combines a number of important measures that dividend investors focus on.

- Yield and History: The company provides a dividend yield of 2.19%, which is appealing next to both the industry average of 0.77% and the wider S&P 500. More significantly, this yield is supported by a provably dependable past. A.O. Smith has not only paid but also raised its dividend each year for at least ten years, establishing a history of dedication that income investors appreciate.

- Dividend Growth: The average yearly dividend growth over the last five years is a satisfactory 7.16%. This steady growth is a key element for offsetting inflation and raising an investor's passive income flow over many years.

- Payout Durability: Possibly most important is the durability of these payments. A.O. Smith’s payout ratio, the percentage of earnings paid as dividends, is about 36%. This is viewed as a low and careful ratio, showing the company keeps a large part of its profits for reinvestment, debt decrease, or future dividend raises. A low payout ratio offers a key safety buffer, confirming the dividend can be continued even in times of briefly lower earnings.

The Base: Profitability and Financial Soundness

A maintainable dividend is only as sound as the business behind it. This is where the screening requirements for "acceptable profitability and soundness" show their value, and A.O. Smith performs well in both areas, each getting a rating of 8.

Profitability is a clear positive. The company has very good returns on capital, with a Return on Invested Capital (ROIC) of 24.4%, doing much better than most of its competitors in the building products industry. Its profit margin of 14.3% and operating margin of 19.0% are also much higher than average, indicating efficient operations and pricing ability. Sound and increasing margins are necessary because they produce the cash flow that finally pays for dividend payments.

Financial Soundness is similarly solid. The company’s balance sheet is marked by very little debt, with an extremely low Debt-to-Equity ratio of 0.06. Its Altman-Z score, a gauge of bankruptcy risk, is very good at 8.02. This financial strength means the company is not too dependent on debt markets and has plenty of room to handle economic changes without putting its dividend at risk. While some liquidity ratios (like the Quick Ratio) are mentioned as points of relative softness, the report explains this by saying the company’s better solvency and profitability probably lessen any short-term liquidity issues.

Valuation and Growth Points

From a valuation viewpoint, A.O. Smith seems fairly valued. Its Price-to-Earnings (P/E) ratio of 16.5 is somewhat less expensive than both the S&P 500 average and its industry competitors. This implies the market is not paying too much for the company’s quality and income flow.

The main area of warning mentioned in the full fundamental report is growth. Both recent revenue growth and future earnings growth projections are in the low-to-mid single digits. Also, the report states the growth rate is slowing. For a pure growth investor, this would be a notable negative. However, for a dividend investor focusing on stability, dependable income, and sound financials, a slower-growth, established company like A.O. Smith can still be an interesting part of a varied income portfolio. The high profitability and clean balance sheet supply the stability that backs the dividend, even in a slower growth setting.

Summary

For investors using a screen that selects for high dividend quality together with profitability and soundness, A.O. Smith offers an example of fit. It provides a yield that is better than average, supported by ten years of growth and a careful payout ratio. This income flow is backed by a very profitable business model and an extremely sound balance sheet. While its growth outlook is limited, the company’s basic positives are exactly the features that help confirm the durability of its dividend over many years, which is the main objective for many income-focused methods.

This review of A.O. Smith was obtained from a methodical screening process. Investors wishing to investigate other companies that fit similar requirements for sound dividends, profitability, and financial soundness can see the full screen results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.