For investors looking for a dependable source of passive income, a methodical selection process is needed to distinguish truly lasting dividend payers from those with uncertain, high yields. One useful method involves selecting for companies that not only rate well on specific dividend measures but also display sound basic financial condition and earnings power. This method focuses on the lasting durability of the payment over seeking the biggest current yield, trying to assemble a collection of companies able to keep and raise their dividends through different economic periods. A stock that results from this strict process is Accenture PLC, Class A (NYSE:ACN), a worldwide professional services frontrunner.

Dividend Profile: A Mix of Yield and Increase

Accenture makes a strong argument for dividend-oriented investors, mainly because of its good and steady history. The company's present dividend yield is about 3.05%, which is especially appealing next to both the wider S&P 500 average and its competitors in the IT Services field. This yield has grown more noticeable after a major drop in share price over the last several months, a circumstance that always requires close examination. However, different from companies where a high yield indicates trouble, Accenture's payment is supported by a record of steadiness and increase.

- Steady History: The company has provided dividends for at least ten years and has not cut its payment in the last five years. This steadiness is a fundamental part of dividend investing, as it shows management's dedication to giving capital back to shareholders.

- Notable Increase: Maybe more notable is the dividend's increase speed. On average, Accenture has raised its yearly dividend by more than 13% over the past five years, a speed that greatly exceeds inflation and adds importantly to total investor gain over time.

For a dividend increase plan, this mix of a reasonable beginning yield and a high increase speed is especially effective, as it lets the income produced from the investment grow substantially over many years.

Evaluating Dividend Durability

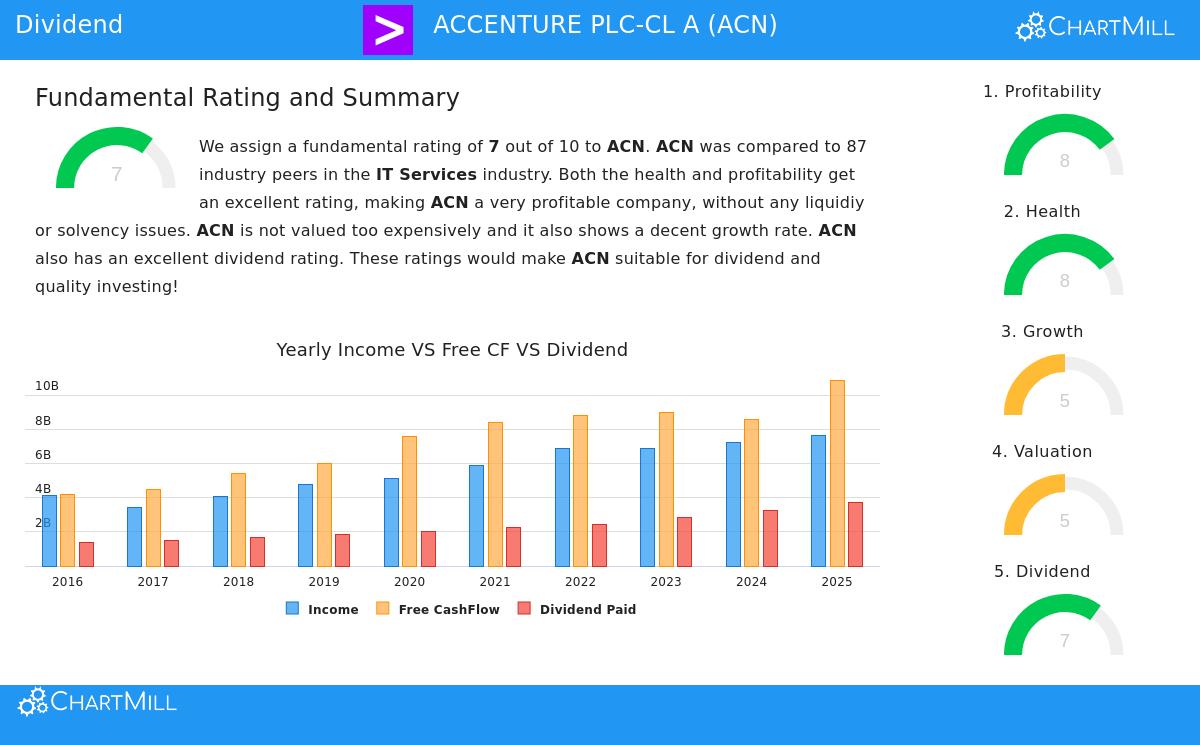

A high yield and increase speed are unimportant if they are not durable. This is where including earnings and condition checks in the selection standards becomes important. Accenture's basic report shows zones of both advantage and concern about its payment's future.

- Payout Ratio: The company pays out about 50% of its net profit as dividends. This is somewhat high but usually stays within a workable area, showing that a large part of earnings is still kept for putting back into the business.

- A Main Point to Consider: The report states that Accenture's earnings are now increasing at a lower speed than its dividend. This difference is a note for durability, implying that the recent double-digit dividend increase might need to slow to match more closely with profit increase in the future years. This shows why a selection that looks past the dividend rating by itself is wise; it requires an investor to inspect the basic engine financing those payments.

Basic Soundness: Earnings Power and Financial Condition

The durability of any dividend finally depends on the company's operational and financial base. This is why the selection plan requires acceptable scores in earnings and condition, to make sure the dividend is not being paid from borrowed time or obligations. Accenture is very good in these zones, which supports trust in its ability to keep its investor returns.

Earnings Power Advantage: Accenture receives a high ChartMill Earnings Power Rating of 8, showing outstanding effectiveness in creating returns from its assets and equity.

- Its Return on Invested Capital (ROIC) of almost 19% is with the best in its field, showing it creates significant value above its capital cost.

- The company keeps good and steady profit and operating margins, which supply a dependable flow of earnings from which dividends can be paid.

Financial Condition Soundness: With a ChartMill Condition Rating of 8, Accenture displays a very firm balance sheet.

- The company has a low Debt/Equity ratio and a very strong Debt to Free Cash Flow ratio, meaning it could in theory pay all its obligations in a few months using its cash flow. This high level of ability to pay is a major protection during economic declines.

- While its present and fast liquidity ratios are typical for its field, they are judged with its excellent ability to pay and earnings power, suggesting the business model does not need too much short-term liquidity.

Valuation Setting

For dividend investors intending to hold for many years, entry price still has importance. Accenture seems fairly priced, trading at a P/E ratio that is a reduction compared to both the general market and its field average. Its price based on cash flow measures also looks appealing next to competitors. This implies investors are not paying extra for the dividend, and might be getting a quality asset at a fair price.

A Subject for More Examination

Accenture PLC comes forward as a significant subject for dividend investors using a complete selection method. It provides a wanted mix of yield and historical increase, backed by first-class earnings power and a very firm financial base. The main point for more careful study is the matching of future dividend increase with earnings increase. Investors should watch management's capital distribution plan to make sure the payment stays durable.

This review of Accenture was prompted by an organized search for quality dividend payers. You can examine the full "Best Dividend Stocks" selection and view other companies that satisfy these strict standards yourself here.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or a bid or request to buy or sell any securities. The review is based on given information and basic reports, which depend on past results and guesses that are not promises of future outcomes. Investors should do their own complete study and think about their personal money situation and risk comfort before making any investment choices.