For investors looking to create passive income, a systematic selection process is necessary to find companies that provide not only a high yield, but a reliable and increasing dividend. One useful approach includes sorting for stocks that receive high marks on a combined dividend score, which examines elements such as yield, increase, and payment reliability, while also checking the core business is fundamentally strong. This involves demanding satisfactory marks for earnings power, to verify the company generates sufficient funds to finance its distributions, and balance sheet strength, to judge its capacity to endure economic weakness without threatening the dividend.

United Parcel Service, Inc. (NYSE:UPS) appears from such a filter as a notable option for dividend-oriented portfolios. The worldwide logistics leader, a central part of the supply chain, presents a situation where a long-standing dependable dividend plan is supported by a solid, though presently pressured, operational framework.

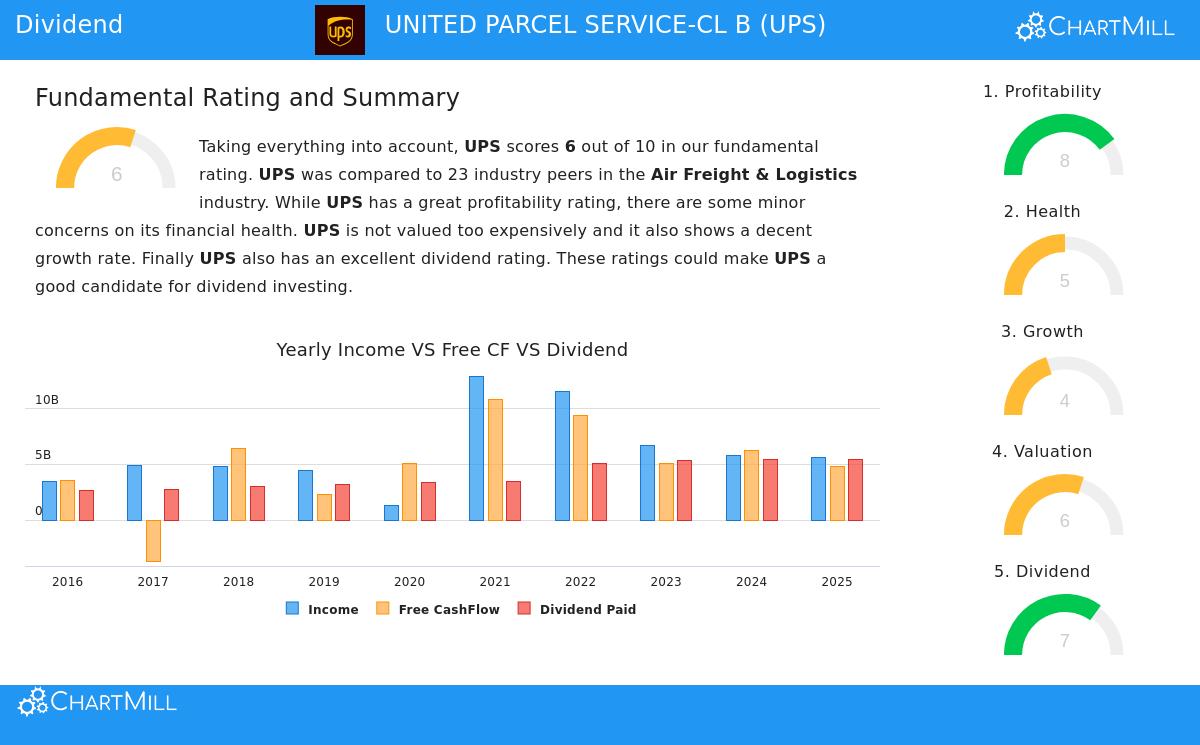

Dividend Attraction: Yield and Increase

For income investors, the initial focus is frequently the yield, and UPS offers a notable one. The company's present dividend yield is at a noticeable 5.86%, which is considerably above both the S&P 500 norm and the wider air freight & logistics sector. This high yield draws attention, but it is the supporting record that adds trust.

- Dependable History: UPS has been distributing and, critically, raising its dividend for more than ten years. This confirms it as a consistent payer, not one that reduces its dividend at the initial hint of difficulty.

- Notable Increase Rate: The dividend has risen at a notable yearly rate of about 10% over the last five years. This increase is a vital element for offsetting inflation and building an investor's income over time.

Judging Dividend Reliability

A high yield and notable increase are irrelevant if they are not reliable. This is where the fundamental review becomes key, and the detailed ChartMill fundamental report for UPS notes both positive points and a main area for observation.

The principal worry for dividend reliability at UPS is its payout ratio. Presently, the company is distributing almost 97% of its earnings as dividends. This is a very high percentage that allows minimal flexibility. If earnings were to fall, continuing the present dividend distribution could rapidly become difficult. This high percentage is a direct consequence of recent pressures on earnings, which highlights why the filter's extra requirements for earnings power and strength are so important.

Foundational Soundness: Earnings Power and Balance Sheet Strength

Despite the high payout ratio, UPS satisfies the filtering standards of "satisfactory earnings power and strength," which supplies a foundational case for the dividend's short-term safety.

- Earnings Power Soundness: UPS receives a high earnings power mark (8 out of 10). Important measures like Return on Equity (34.34%) and Profit Margin (6.28%) place it with the leading companies in its sector. This shows the core operation is very efficient and produces significant earnings from its activities—the required source for any dividend.

- Satisfactory Balance Sheet Strength: The company's strength mark (5 out of 10) is adequate, though it shows some debt. The Altman-Z score indicates no close bankruptcy danger, and the debt amounts, while increased, are workable compared to the company's cash generation. The liquidity measures (Current and Quick Ratio) are satisfactory, showing UPS can fulfill its immediate responsibilities. This basic level of financial steadiness is essential for a reliable dividend stock, as a company under financial pressure is often compelled to reduce its distribution.

Price and Expansion Background

From a price standpoint, UPS seems fairly valued. Its Price-to-Earnings ratio is under both the market and sector norms, indicating the market has already accounted for present difficulties. Looking forward, analysts forecast a return to earnings expansion, which, if achieved, would naturally better the worrying payout ratio over time. This possibility for improving expansion is a main element that could aid future dividend raises.

A Measured Perspective for Dividend Investors

UNITED PARCEL SERVICE-CL B (UPS) offers a detailed possibility for dividend investors. It provides a high, well-supported yield from a profit-generating business with an excellent record of yearly raises. The main caution is the strained payout ratio, which requires close watching of the company's earnings path. However, the filter's system—which required good earnings power and satisfactory strength—helps recognize that UPS possesses the basic operational soundness and financial durability to manage this phase. It is not a company with a failed model, but instead one experiencing a periodic decline.

For investors at ease with some periodic change and who trust the long-term need for global logistics, UPS represents a method to obtain a high initial yield from an established company, with the chance for expansion as the operation improves. As usual, it should be viewed as part of a varied income portfolio.

Interested in examining other stocks that meet this systematic dividend filter? You can inspect the complete list and modify the settings to your own standards via the Best Dividend Stocks screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.