For investors looking to balance the attraction of fast increase with the caution of sensible prices, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" method presents a practical middle path. This method tries to find companies that are producing good, lasting increase and are also available at prices that do not require extreme future success. It avoids the speculative excitement often seen around high-rising tech stocks while staying clear of cheap stocks in slow-moving fields. By concentrating on businesses with good basics, including sound financial statements and steady earnings, together with appealing increase paths, this method aims to create a collection set up for lasting gains with a controlled amount of risk.

A recent search using an Affordable Growth filter, which selects for stocks with high increase grades, acceptable earnings and financial soundness, and fair prices, identified Workday Inc. (NASDAQ:WDAY) as a candidate for more review. The supplier of business cloud software for finance and human resources shows several main traits that match the GARP idea.

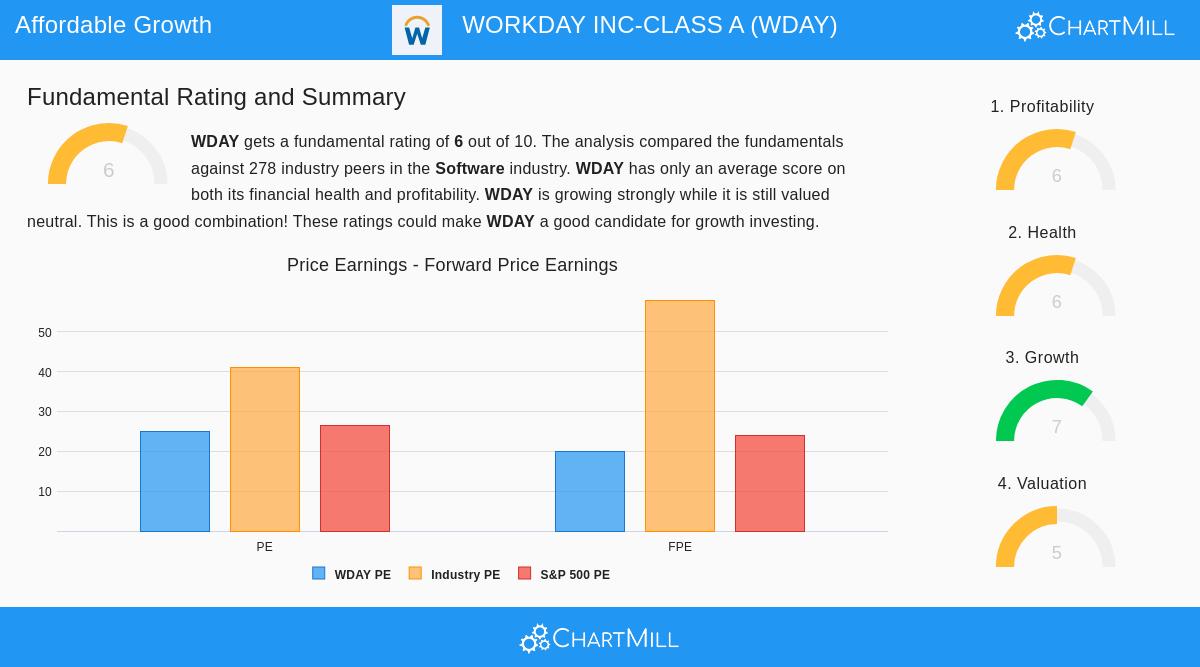

A Closer Look at the Fundamental Picture

A full fundamental analysis report for Workday gives a measured look across five important sections: Increase, Price, Soundness, Earnings, and Dividend. The company's total fundamental grade of 6 out of 10 puts it in a good, though not outstanding, place compared to other software industry companies. The details of its grades tell a more detailed story that is key to the affordable increase idea.

- Overall Fundamental Grade: 6/10

- Increase Grade: 7/10

- Price Grade: 5/10

- Soundness Grade: 6/10

- Earnings Grade: 6/10

- Dividend Grade: 0/10

Increase: The Core Engine

The increase section is where Workday does best, getting a grade of 7. This score is the main reason for its place in an affordable growth filter and shows good past speed along with positive future views.

- Past Results: The company has shown notable enlargement, with Earnings Per Share (EPS) rising by 24.89% over the last year and at a yearly speed of 30.89% over recent years. Sales increase has also been strong, going up 13.16% last year and 18.42% each year over a longer time.

- Future View: Experts expect this speed to keep going, though at a somewhat slower rate. EPS is thought to rise by 17.80% yearly, while sales is predicted to go up by 12.58% on average. This expected slowing from past very fast increase is normal for established software leaders but is still "quite good," as per the analysis, and forms a believable base for future price.

For the GARP investor, this mix of shown results and a believable increase path is necessary. It suggests the company is progressing past its first high-change increase stage into a time of more lasting, predictable enlargement.

Price: The "Reasonable Price" Check

With a price grade of 5, Workday is in a middle area, which is exactly what the affordable growth method looks for, companies that are not extremely overpriced relative to their chances. The analysis shows a varied but finally fair picture.

- Absolute vs. Relative Price: Workday's Price-to-Earnings (P/E) ratio of 24.98 and Forward P/E of 19.87 are called "rather high" on their own. However, setting is key. Compared to the software industry's average, Workday costs less than about 74% of similar companies based on forward earnings. Its Enterprise Value/EBITDA and Price/Free Cash Flow ratios also show it is priced lower than most of the industry.

- Increase Adjustment: Maybe most key for increase investors, the analysis states that Workday's low PEG ratio, which changes the P/E for increase, "shows a rather low price of the company." This measure directly relates to the GARP idea, suggesting the market may not be fully counting the company's increase potential.

This price picture backs the method's aim: avoiding the highest-cost names in a popular area while still taking part in a leader with a good increase profile.

Supporting Fundamentals: Soundness and Earnings

An affordable increase stock cannot depend on increase only, it needs a steady base. Workday's middle grades in Financial Soundness (6) and Earnings (6) give that needed support, showing there are no major warning signs that could stop the increase story.

- Financial Soundness: The company keeps a good financial statement. Its Altman-Z score suggests no failure risk, and a very low debt-to-free-cash-flow ratio of 1.16 shows strong ability to pay. While its debt-to-equity ratio is higher than some similar companies, the report states this is well-managed by good cash flow. Cash measures like the Current and Quick Ratios are at normal, good levels.

- Earnings: Workday is solidly earning money. Its Return on Equity (13.62%) and Return on Invested Capital (9.29%) do better than over 80% of the software industry. Margins are a specific strength, with both Operating Margin (15.55%) and Profit Margin (13.10%) placed in the top group of similar companies and showing gain.

These points are important for the method because they lower risk. A company with poor financial soundness or weak earnings might find it hard to pay for its increase from within or could be at risk during economic slowdowns, making its increase path less dependable.

Conclusion and Further Research

Workday Inc. shows an example of the kind of company aimed for by an affordable growth filter. It has a good, provable increase engine, both in its recent past and its expected future, which is the main draw. Importantly, this increase is not priced at a very high level when seen within its competitive industry and changed for its increase rate, meeting the "reasonable price" need. Also, acceptable grades in financial soundness and earnings suggest the company has the operational steadiness and earning ability to possibly maintain its enlargement.

It is good to know that, like most increase-focused tech firms, Workday does not give a dividend, sending its cash flow instead toward reinvestment and increase projects.

For investors wanting to look at other companies that match this balance of increase, price, and fundamental strength, you can find more results from this Affordable Growth filter here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any securities. Investing has risk, including the possible loss of the original amount. Readers should do their own study and talk with a qualified financial advisor before making any investment choices.